Autonomous vehicles (AVs) are everywhere in headlines — and yet surprisingly hard to pin down in reality. Announcements, pilots, and promises multiply, but for cities, transit agencies, and regulators, a simple question remains difficult to answer: Which autonomous vehicles are actually operating today — and what services do they provide?

Download the AV use-case overview

Q1 2026 edition of the Autonomous Driving Systems Use Cases

I developed this overview through my work at Urban Innovate, where I advise on AV readiness and operate at the intersection of autonomous vehicles, public transport, and urban policy, with hands-on experience in research, deployments, regulation, and large-scale pilots across Europe, the U.S., and Asia.

This mapping is intended as a practical reference and living document. It can be used by cities, transit agencies, regulators, and industry stakeholders to understand the current landscape of autonomous services and identify where autonomy is already delivering operational value versus where it remains experimental.

Automated vs. autonomous: a terminology gap

To determine whether a service is included in this mapping, we use a liability-based definition of autonomy. A vehicle or service is considered autonomous when, under defined operating conditions, responsibility for the driving task shifts from a human driver to the vehicle manufacturer or the Autonomous Driving System (ADS) provider.

Throughout this document, autonomy is described using the SAE International levels of driving automation (SAE J3016). While imperfect, this framework remains the most practical and broadly accepted reference. In this context, the mapping focuses on SAE Levels 3 and 4, where the ADS performs the driving task under specific and limited conditions. We therefore focused on:

- Services that have obtained a commercial permit, or

- Services operating under exemptions or test permits, but that have reached a level of technical and operational maturity suggesting a credible path to scaled deployment.

Throughout this document, I use both the terms autonomous and automated. In the U.S., driverless robotaxi operations are commonly described as autonomous, while in Europe the term automated is preferred, reflecting a regulatory and operational

focus on the progressive transfer of driving tasks from the safety driver to the ADS.

Credits: Autonomy Paris

What this overview covers — and what it does not

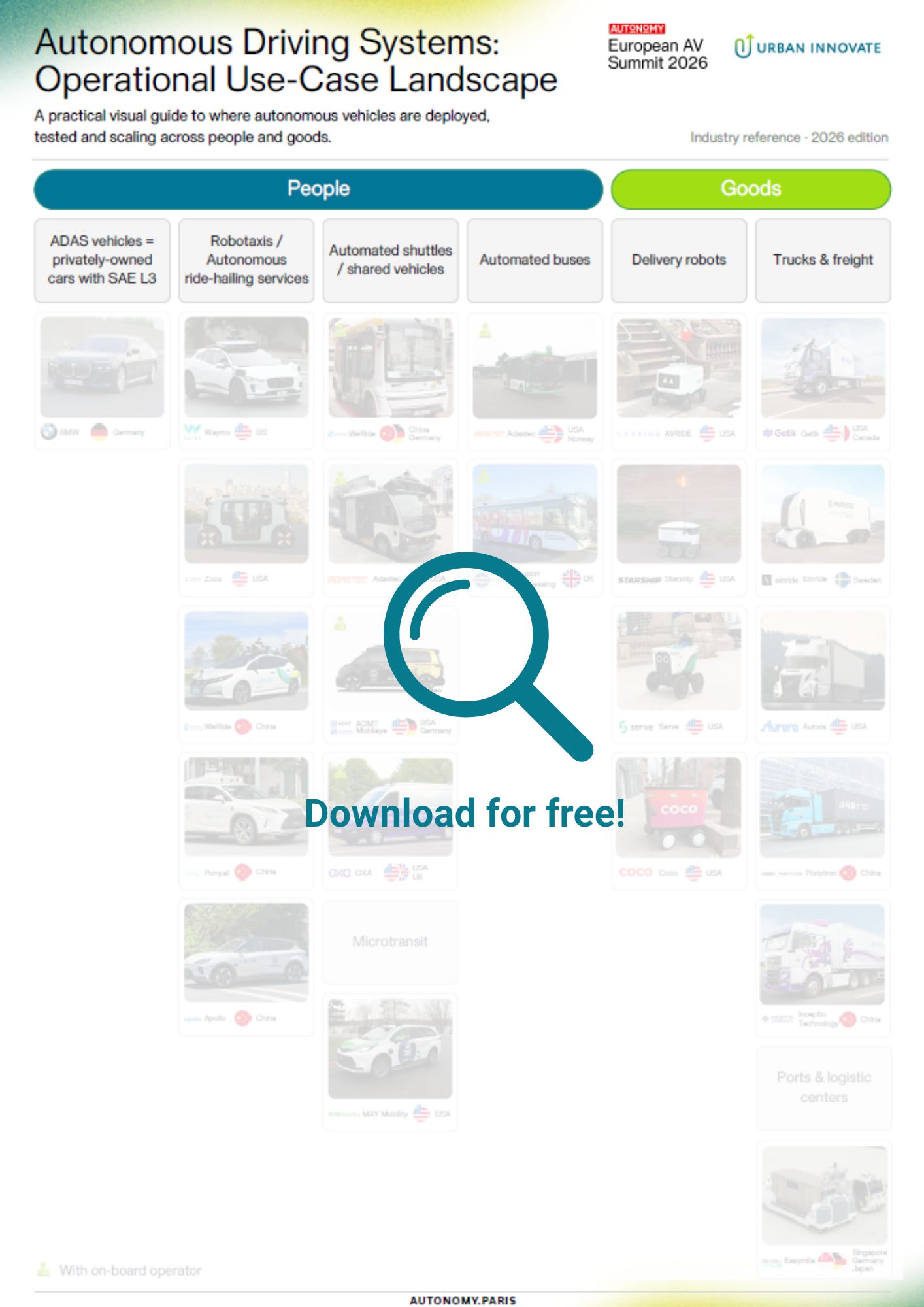

The mapping covers the following services (also called ‘use cases’):

- Passenger cars with SAE L3 capabilities with their Advanced Driver Assistance Systems (ADAS)

- Robotaxis

- Automated shuttles and microtransit services

- Automated buses

- Delivery robots

- Trucks and port operations

Services operating on segregated or dedicated lanes — such as Glydways and 2getthere — are intentionally excluded. While highly relevant, they are closer, conceptually and operationally, to automated trams or light rail than to mixed-traffic autonomous vehicles. Furthermore, prototypes intended for future road operation are also excluded, as is urban air mobility (UAM).

Finally, this mapping focuses on ADS providers, sometimes in combination with vehicle manufacturers. It does not cover the critical role of operators — whether global players such as Transdev or regional ones like De Lijn in Belgium — nor mobility service providers such as beep, MOIA, or Via. This dimension is intentionally left for a separate article.

Three dominant pathways toward vehicle autonomy

While private car ownership models still target individual consumers and unit sales, I am convinced that the most transformative impacts are expected from shared services in the form of shared assets (robotaxis) and shared rides (shuttles and buses), as well as autonomous delivery and freight services.

Passenger cars: from advanced driver assistance to conditional autonomy

While fully autonomous robotaxis capture headlines, the immediate economic engine of the ADS industry lies in the massive volume of private passenger cars sold annually. Today, all major manufacturers offer SAE Level 2 systems (e.g., adaptive cruise control), where the driver remains responsible. While SAE Level 3 represents a major leap by transferring liability to the manufacturer, the industry is witnessing a strategic retreat from this pathway: Mercedes-Benz has paused L3 availability to refocus on L2; General Motors has reallocated resources to its profitable Super Cruise (L2) following setbacks with its L4 Cruise robotaxi fleet; and Tesla’s Full Self-Driving (FSD) remains an SAE Level 2 system without L3 permits — illustrating a broader industry trend of maximizing driver assistance while avoiding the regulatory and liability mire of higher automation.

Robotaxis: the most visible — but not the only — autonomous service

Robotaxis dominate public attention, and for good reason: they are the most advanced and visible form of autonomous driving in mixed traffic today, capturing the vast majority of industry funding — underscored by the staggering $43 billion cumulatively invested in leaders like Waymo, Pony.ai, and WeRide. Waymo remains the global reference, with more than 100 million autonomous miles driven by the end of 2025 and a $16 billion funding round in early 2026. In China, Pony.ai and WeRide have reached a similar level of maturity. By contrast, Tesla is still in a transitional phase: as of February 2026, it has begun limited unsupervised operations in Austin (invite-only, no safety driver) while San Francisco still mandates a safety driver. Wayve and Motional, not included in this mapping, remain companies to watch.

Automated shuttles & microtransit — where autonomy matters most for transit

Shared autonomy is, in my opinion, transit’s biggest opportunity, yet most fleets remain tethered to onboard safety operators due to persistent permitting and liability hurdles — with the exception of May Mobility, which still seems to operate driverless microtransit services in Ann Arbor. However, the “slow shuttle” era is finally fading; my firsthand experience with WeRide’s deployment for De Lijn in Leuven, Belgium, reveals a new wave of systems capable of much more fluid operation. Mobileye occupies a distinctive position, integrated into platforms such as HOLON and the VW ID. Buzz. Notably, no clear signals have emerged that Waymo or Zoox plan to introduce pooling or shared rides, while VW ADMT via MOIA already operates pooled services in Hamburg.

Autonomous buses: high expectations, harsh market realities

Clients frequently ask: “What about autonomous buses?” The answer is a collision of high-tech potential and low-budget reality. While driver shortages are reaching a breaking point, the market remains stalled by prohibitive technology costs, rigid procurement cycles, and transit budgets already drained by fleet electrification — plus political friction. For now, the real momentum is behind the scenes in depot automation: previous research I coordinated with EMT Madrid proved that automating “non-revenue” tasks — washing, charging, and repositioning — frees drivers for the road while slashing operational costs. Projects like CapMetro’s “YARD” program in Austin, alongside WSP, are proving that the most viable path for bus autonomy starts in the depot, not on the street.

Delivery sidewalk robots: innovation or obstacle?

Small-scale autonomy has arrived on the sidewalk. Companies like Starship and Serve Robotics have deployed thousands of delivery robots across the U.S., but their true value proposition is under fire: it’s still unproven whether they reduce traffic congestion or merely shift the burden of delivery from the asphalt to the pavement. The friction is real — from blocking wheelchair ramps to awkward standoffs with cyclists. Meanwhile, China has largely moved toward larger, road-legal delivery pods that prioritize volume over sidewalk interaction.

The heavyweights: trucks, ports, and the freight frontier

While robotaxis win the PR war, autonomous trucking is where the “heavy metal” meets the road. In North America, endless highways and a chronic driver shortage have turned long-haul freight into the ultimate proving ground. Waabi recently made waves with a $750 million Series C, proving that the software “brains” for a 40-ton semi and a passenger car are rapidly converging. However, the “driverless” claim in freight often comes with an asterisk: verifying whether a “safety pilot” is actually behind the wheel or monitoring remotely is notoriously difficult. And don’t overlook ports and closed-loop freight hubs — these controlled environments are the secret laboratories where the ADS stacks of the future are perfected.

Acknowledgement, limitations, and how to read this document

As of February 2026, this overview synthesizes public data, expert insights, and firsthand experience across the U.S., Europe, and Asia. While I have aimed for technical accuracy, some subjectivity is inevitable when assessing “real-world” autonomy and human intervention levels. A current limitation is the UAE and Middle East; despite their high activity, limited direct exposure prevents comprehensive coverage in this version. This is a living document designed to evolve alongside the industry. Feedback, corrections, and new deployment data are actively encouraged for future updates!